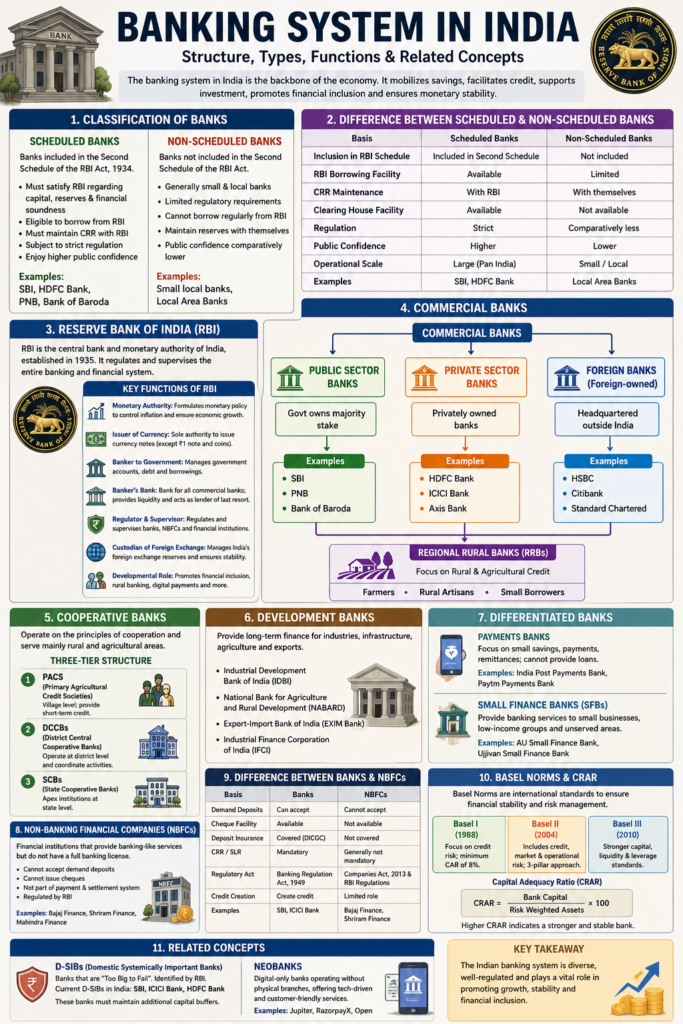

The Banking System in India forms the backbone of the country’s financial and economic structure. It mobilizes savings, facilitates credit creation, supports investment, promotes trade and commerce, and ensures the smooth flow of money across the economy. From financing industries and agriculture to enabling digital payments and financial inclusion, banks play a central role in India’s development process.

In a developing economy like India, the banking sector performs not only economic functions but also social and developmental functions. It helps implement welfare schemes, expands financial access to weaker sections, supports rural development, and strengthens monetary stability.

Over the years, the Indian banks has evolved into a diversified and technology-driven financial ecosystem consisting of commercial banks, cooperative banks, development banks, differentiated banks, NBFCs, and digital banking institutions functioning under the supervision of the Reserve Bank of India.

What is the Banking System?

The bank system refers to the organized network of financial institutions that provide banking and financial services to individuals, businesses, and governments.

The major activities of banks include:

- Accepting deposits

- Providing loans and advances

- Facilitating payments and remittances

- Mobilizing savings

- Creating credit

- Supporting investment and production

Banks act as financial intermediaries by transferring funds from surplus units (savers) to deficit units (borrowers). This process promotes capital formation, investment, employment generation, and economic growth.

Thus, the banks act as the financial lifeline of the economy.

How Banking in India has evolved?

This has evolved through multiple phases in India.

Early Banking:

Ancient India witnessed informal banking activities through moneylenders, merchants, and indigenous banking communities.

Colonial Period:

Modern banking began during British rule with the establishment of:

- Bank of Bengal

- Bank of Bombay

- Bank of Madras

These later merged to form the Imperial Bank of India, which eventually became State Bank of India.

Post-Independence Phase:

After independence, India adopted planned economic development, and banks were used as instruments of socio-economic transformation.

Major developments included:

- Nationalization of banks

- Expansion of rural banking

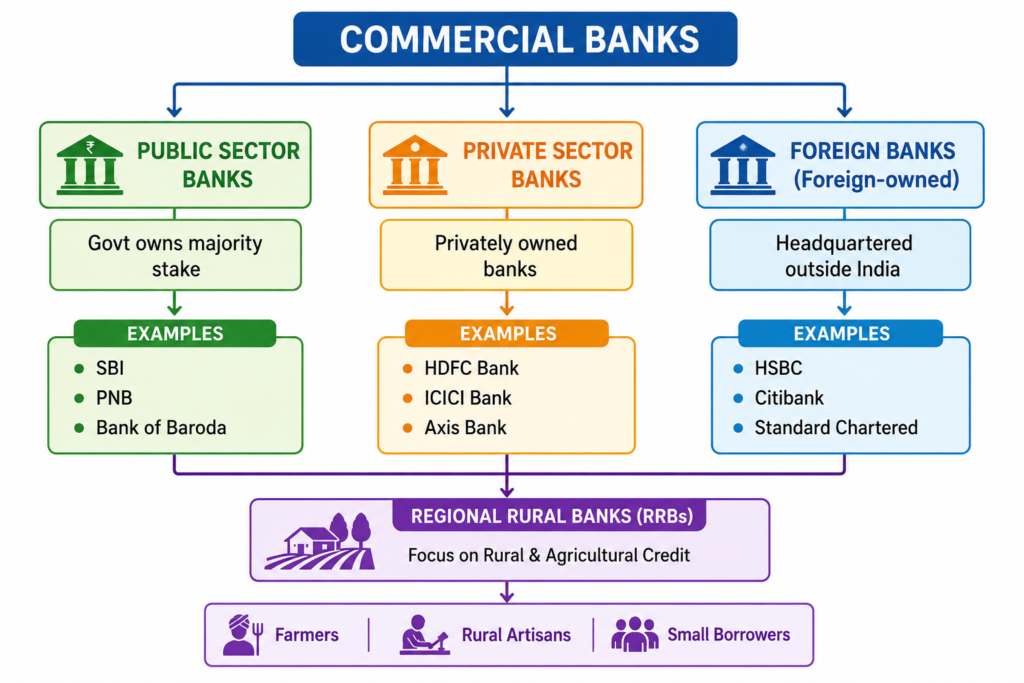

- Creation of Regional Rural Banks

- Priority Sector Lending

- Agricultural finance expansion

Liberalization Era (Post-1991)

Economic reforms transformed Indian banking through:

- Entry of private banks

- Increased competition

- Technological modernization

- Digital banking growth

- Financial sector reforms

Today, India possesses one of the world’s largest banking networks.

How are Banks classified in Indian Financial system?

Banks in India are broadly classified into:

- Scheduled Banks

- Non-Scheduled Banks

This classification is based on their inclusion in the Second Schedule of the RBI Act, 1934.

- Scheduled Banks

Scheduled Banks are banks included in the Second Schedule of the RBI Act, 1934.

To qualify as a scheduled bank, an institution must satisfy RBI regarding:

- Financial soundness

- Capital adequacy

- Depositor protection

Features of Scheduled Banks:

- Eligible to borrow from RBI

- Members of clearing house facilities

- Subject to stricter RBI regulation

- Must maintain CRR with RBI

- Enjoy higher public confidence

Scheduled banks dominate the Indian banking sector and handle most banking transactions in the economy.

Examples:

- State Bank of India

- HDFC Bank

- Punjab National Bank

- Non-Scheduled Banks

Non-Scheduled Banks are banks not included in the Second Schedule of the RBI Act.

These banks generally:

- Operate on a smaller scale

- Serve local or regional areas

- Possess limited financial resources

Though regulated by RBI, they do not enjoy all facilities available to scheduled banks.

Their role has gradually declined with the expansion and consolidation of modern banking institutions.

What Are The Differences Between Scheduled and Non-Scheduled Banks?

| Basis | Scheduled Banks | Non-Scheduled Banks |

| Meaning | Included in Second Schedule of RBI Act | Not included in Second Schedule |

| RBI Borrowing | Can borrow regularly from RBI | Limited borrowing facility |

| Regulation | Strict RBI supervision | Comparatively less regulation |

| CRR Maintenance | Maintain CRR with RBI | Maintain reserves with themselves |

| Clearing House Facility | Available | Not available |

| Public Confidence | Higher | Comparatively lower |

| Operational Scale | Large-scale operations | Mostly local operations |

| Examples | SBI, HDFC Bank | Small local banks |

What is the Structure of Banking System in India?

The Indian banking system has a multi-layered institutional structure.

Main Components:

- Reserve Bank of India (RBI)

- Commercial Banks

- Cooperative Banks

- Development Banks

- Differentiated Banks

- Non-Banking Financial Companies (NBFCs)

What is the Reserve Bank of India (RBI)?

The Reserve Bank of India is the apex institution of India’s banking and monetary system. Established in 1935, RBI regulates and supervises the entire financial system of the country.

RBI acts as:

- Central bank of India

- Banker to the government

- Banker’s bank

- Monetary authority

- Custodian of foreign exchange reserves

The RBI plays a crucial role in maintaining financial stability, public confidence, and monetary discipline.

Functions of RBI:

1. Monetary Authority

RBI formulates and implements monetary policy to:

- Control inflation

- Maintain price stability

- Regulate money supply

- Support economic growth

It uses instruments like:

- Repo Rate

- Reverse Repo Rate

- CRR

- SLR

- Open Market Operations

2. Issuer of Currency:

RBI has the sole authority to issue currency notes in India except the ₹1 note and coins.

It ensures:

- Adequate currency supply

- Security of currency system

- Clean note circulation

3. Banker to Government:

RBI manages banking transactions of Central and State Governments.

Its functions include:

- Maintaining government accounts

- Managing public debt

- Handling government borrowings

- Facilitating receipts and payments

4. Banker’s Bank

RBI acts as the bank for all commercial banks.

It:

- Maintains reserves of banks

- Provides emergency liquidity

- Facilitates interbank settlements

- Supervises banking activities

Hence, RBI is called the “Lender of Last Resort.”

5. Regulator and Supervisor:

RBI regulates:

- Commercial banks

- Cooperative banks

- NBFCs

- Payment banks

Its objective is to ensure:

- Stability of banking system

- Protection of depositors

- Financial discipline

6. Custodian of Foreign Exchange:

RBI manages India’s foreign exchange reserves under FEMA, 1999.

It ensures:

- Stability of Indian rupee

- Smooth foreign exchange operations

- External sector stability

7. Developmental Role:

RBI also promotes:

- Financial inclusion

- Rural banking

- Digital payment systems

- Institutional credit expansion

Thus, RBI performs both regulatory and developmental functions.

What are Commercial Banks?

Commercial Banks are profit-oriented financial institutions that accept deposits and provide loans to individuals, businesses, and governments.

They form the core of the Indian banking system and play a major role in:

- Credit creation

- Capital formation

- Trade facilitation

- Economic growth

Structure of Commercial Banks

Features of Commercial Banks:

- Accept deposits from public

- Provide loans and advances

- Facilitate digital transactions

- Create credit in economy

- Promote trade and investment

- Operate mainly on profit motive

Commercial banks are the backbone of the modern financial system.

What are Cooperative Banks?

Cooperative banks function on the principles of:

- Cooperation

- Mutual assistance

- Democratic management

They mainly cater to:

- Farmers

- Rural households

- Small traders

- Cooperative societies

Three-Tier Cooperative Structure of Cooperative Banks:-

Primary Agricultural Credit Societies (PACS)

Village-level cooperative institutions providing short-term agricultural credit.

District Central Cooperative Banks (DCCBs)

Coordinate cooperative banking activities at district level.

State Cooperative Banks (SCBs)

Apex cooperative institutions operating at state level.

Cooperative banks play an important role in rural credit and agricultural development.

What are Development Banks?

Development Banks provide long-term finance for industries, infrastructure, agriculture, and exports. Unlike commercial banks, they focus more on developmental objectives than short-term profits.

Major Functions:

- Infrastructure financing

- Industrial development

- Agricultural support

- Export promotion

- Entrepreneurship development

Major Development Banks

- NABARD

- EXIM Bank

- Industrial Development Bank of India

Development banks significantly contributed to India’s industrialization and rural development.

What are Differentiated Banks?

Differentiated banks are specialized banks established to fulfill specific financial objectives and improve financial inclusion.

- Payments Banks

Payments banks focus on:

- Small savings

- Digital payments

- Remittances

- Financial inclusion

They cannot provide large-scale loans.

Examples:

- India Post Payments Bank

- Paytm Payments Bank

- Small Finance Banks (SFBs)

Small Finance Banks provide banking services to:

- Small businesses

- Marginal farmers

- Low-income households

- Informal sector workers

Examples:

- AU Small Finance Bank

- Ujjivan Small Finance Bank

They help deepen financial inclusion at the grassroots level.

| Basis | Payments Banks | Small Finance Banks (SFBs) |

| Main Objective | Promote digital payments, remittances, and small savings | Provide banking and credit facilities to small borrowers and weaker sections |

| Lending Facility | Cannot provide loans | Can provide loans and advances |

| Target Groups | Migrant workers, low-income users, small savers | Small farmers, MSMEs, informal sector, low-income households |

What are Non-Banking Financial Companies (NBFCs)?

NBFCs are financial institutions that perform banking-like functions without possessing a full banking license.

They provide:

- Loans

- Leasing

- Investment services

- Consumer finance

- Microfinance

NBFCs complement traditional banks by serving sectors often neglected by formal banking institutions.

Features of NBFCs:

- Cannot accept demand deposits

- Cannot issue cheques

- Not part of payment settlement system

- Regulated mainly by RBI

NBFCs are especially important in MSME financing and rural credit delivery.

What are the Differences Between Banks and NBFCs?

| Basis | Banks | NBFCs |

| Meaning | Full-fledged banking institutions | Financial institutions with limited banking functions |

| Demand Deposits | Can accept | Cannot accept |

| Cheque Facility | Available | Not available |

| Payment System | Part of settlement system | Not part of payment system |

| Deposit Insurance | Covered under DICGC | Usually not covered |

| CRR & SLR | Mandatory | Generally not mandatory |

| Regulation | Banking Regulation Act | Companies Act + RBI rules |

| Credit Creation | Direct role | Limited role |

| Examples | SBI, ICICI Bank | Bajaj Finance, Shriram Finance |

NBFCs play a complementary role by expanding financial access to underserved sectors.

What are Basel Norms:

The Basel Norms are international banking regulations developed by the Basel Committee on Banking Supervision to strengthen banking stability and risk management globally.

Basel I:

Focused mainly on:

- Credit risk

- Minimum capital adequacy standards

Basel II:

Expanded regulation to include:

- Credit risk

- Market risk

- Operational risk

Introduced the three-pillar framework:

- Capital adequacy

- Supervisory review

- Market discipline

Basel III:

Introduced after the 2008 Global Financial Crisis.

Focused on:

- Stronger capital buffers

- Better liquidity management

- Improved risk resilience

It aimed to strengthen banks against financial shocks.

What is a Capital Adequacy Ratio (CRAR)?

CRAR measures the financial strength and stability of banks.

CRAR=(Bank Capital/Risk Weighted Assets)×100

A higher CRAR indicates a safer and more stable bank.

India follows stricter capital adequacy norms than the global Basel requirement.

What is Financial Inclusion ?

Financial inclusion means ensuring affordable financial services to all sections of society, especially vulnerable groups.

Major initiatives include:

- Jan Dhan Yojana

- UPI ecosystem

- Direct Benefit Transfer (DBT)

- MUDRA loans

- Rural banking expansion

Financial inclusion promotes:

- Poverty reduction

- Women empowerment

- Inclusive growth

- Formalization of economy

What are Domestic Systemically Important Banks (D-SIBs)?

D-SIBs are banks considered “Too Big to Fail” because their collapse can destabilize the economy.

Major Indian D-SIBs:

- State Bank of India

- ICICI Bank

- HDFC Bank

These banks must maintain additional capital buffers.

What are Neo-banks and Digital Banks?

Neobanks are fully digital banking platforms operating without physical branches.

Features

- Mobile-based banking

- Instant onboarding

- AI-enabled services

- Low operational costs

- Personalized financial management

Examples

- Jupiter

- Razorpay

Digital banking is transforming India into a leading digital payment economy.

What are Emerging Trends in Indian Banking?

UPI Revolution

India’s Unified Payments Interface has revolutionized digital payments globally.

Fintech Collaboration

Banks increasingly partner with fintech firms for:

- Faster lending

- Digital payments

- Improved customer experience

Digital Rupee (CBDC)

RBI is exploring Central Bank Digital Currency for secure digital transactions.

Artificial Intelligence in Indian Banks:

AI is increasingly used for:

- Fraud detection

- Customer support

- Credit assessment

- Risk management

Conclusion

The Banking System in India is the financial backbone of the economy. It mobilizes savings, creates credit, facilitates investments, promotes financial inclusion, and ensures economic stability. From traditional branch banking to digital financial ecosystems, Indian banking has undergone remarkable transformation over the decades.

Today, the sector plays a multidimensional role — supporting industries, empowering rural communities, enabling digital transactions, and driving inclusive growth. As India advances toward becoming a major global economic power, the banking system will continue to remain one of the strongest pillars of sustainable economic development.

For more such preparation strategies, you can read here: https://laex.in/category/preparation-strategy/

La Excellence IAS Academy, the best IAS coaching in Hyderabad, known for delivering quality content and conceptual clarity for UPSC 2025 preparation.

FOLLOW US ON:

◉ Youtube : https://www.youtube.com/@CivilsPrepTeam

◉ Facebook: https://www.facebook.com/LaExcellenceIAS

◉ Instagram: https://www.instagram.com/laexcellenceiasacademy/

GET IN TOUCH:

Contact us at info@laex.in, https://laex.in/contact-us/

or Call us @ +91 9052 29 2929, +91 9052 99 2929, +91 9154 24 2140

OUR BRANCHES:

Head Office: H No: 1-10-225A, Beside AEVA Fertility Center, Ashok Nagar Extension, VV Giri Nagar, Ashok Nagar, Hyderabad, 500020

Madhapur: Flat no: 301, survey no 58-60, Guttala begumpet Madhapur metro pillar : 1524, Rangareddy Hyderabad, Telangana 500081

Bangalore: Plot No: 99, 2nd floor, 80 Feet Road, Beside Poorvika Mobiles, Chandra Layout, Attiguppe, Near Vijaya Nagara, Bengaluru, 560040.