Paper: GS – III, Subject: Indian Economy, Topic: Economic Reforms, Issue: Equity in Corporate Insolvency Resolution (CIIRP Reform).

Context:

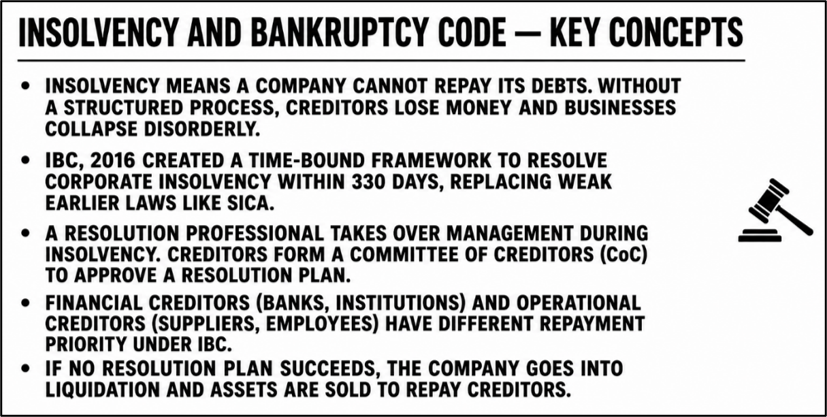

When a company cannot repay its debts, it becomes insolvent. India’s IBC, 2016 created a structured, time-bound process to resolve such situations. The 2026 Amendment introduces Creditor-Initiated Insolvency Resolution Process (CIIRP) as a faster alternative, but its restricted access raises fairness concerns.

Key Takeaways:

Explanation:

1. Core Problem:

- Companies enter markets easily but face long delays when exiting through formal insolvency, called the Chakravyuha Challenge.

- Litigation and procedural gaps slow CIRP (Corporate Insolvency Resolution Process), destroying business value in the process.

- Under CIRP, a Resolution Professional takes over management and creditors form a Committee of Creditors (CoC) to approve a resolution plan.

- If no plan succeeds, the company goes into liquidation and assets are sold to repay creditors.

2. What CIIRP Does:

- Unlike CIRP, where management loses control immediately, CIIRP lets existing management continue under a resolution specialist’s supervision.

- It reduces court involvement, preserves business continuity and enables faster restructuring.

- It is a less disruptive alternative for companies facing short-term financial stress.

3. The Vidarbha Industries Issue:

- Earlier, National Company Law Tribunal (NCLT) could accept or reject insolvency applications even when debt and default were clearly proven.

- The 2026 Amendment replaces “may” with “shall”, making admission compulsory when debt and default are proven through information utility records.

- This protects creditors but may pressure companies facing only temporary cash flow problems.

4. Restricted Access Concern:

- CIIRP can only be started by “notified financial institutions”, creating an unfair hierarchy among creditors.

- Smaller financial creditors and operational creditors are forced into the more aggressive CIRP just to recover money.

- The Swiss Ribbons judgment justified the financial-operational creditor distinction under Article 14, but this new sub-classification within financial creditors lacks similar legal justification.

- Concentrating power in notified institutions weakens Inter-Creditor Agreements and makes restructuring less fair.

5. Way Forward:

- A Universal CIIRP should allow any financial creditor backed by 51% of total financial debt to initiate proceedings.

- This replaces institutional identity with financial exposure as the basis for initiation.

- Both US Chapter 11 and UK Part 26A follow this principle — access based on financial stake, not regulatory status.

Conclusion

India’s insolvency system needs speed, fairness and value preservation. Limiting CIIRP access to select institutions weakens the reform’s broader impact. A universal, exposure-based model can make India’s insolvency framework more balanced and globally competitive.

Source: (The Hindu)

La Excellence IAS Academy, the best IAS coaching in Hyderabad, known for delivering quality content and conceptual clarity for UPSC 2026 preparation.

FOLLOW US ON:

◉ YouTube : https://www.youtube.com/@CivilsPrepTeam

◉ Facebook: https://www.facebook.com/LaExcellenceIAS

◉ Instagram: https://www.instagram.com/laexcellenceiasacademy/

GET IN TOUCH:

Contact us at info@laex.in, https://laex.in/contact-us/

or Call us @ +91 9052 29 2929, +91 9052 99 2929, +91 9154 24 2140

OUR BRANCHES:

Head Office: H No: 1-10-225A, Beside AEVA Fertility Center, Ashok Nagar Extension, VV Giri Nagar, Ashok Nagar, Hyderabad, 500020

Madhapur: Flat no: 301, survey no 58-60, Guttala begumpet Madhapur metro pillar: 1524, Rangareddy Hyderabad, Telangana 500081

Bangalore: Plot No: 99, 2nd floor, 80 Feet Road, Beside Poorvika Mobiles, Chandra Layout, Attiguppe, Near Vijaya Nagara, Bengaluru, 560040